The insurance industry is entering a new phase of operational pressure. Over the past decade, insurers have expanded into new products, digital distribution channels, and more sophisticated risk models.

At the same time, regulatory expectations and customer demands have continued to grow.

The result is a sector that is larger and more dynamic than ever, but also significantly more complex to operate.

According to the Swiss Re Institute Global Insurance Outlook¹, global insurance premiums are expected to exceed $8 trillion in the coming years, reflecting steady growth across life and non-life markets.

Growth, however, brings operational challenges. Many insurers are discovering that their underlying processes were not designed for the scale, speed, and transparency required today.

And in most organizations, two processes sit at the center of this challenge: claims and underwriting.

Source¹: https://www.swissre.com/institute/research/sigma-research.html

Where Operational Complexity Concentrates: Claims and Underwriting

Within insurance operations, claims and underwriting play a uniquely critical role.

Underwriting determines how risk is assessed and priced. It directly influences portfolio quality, profitability, and how quickly insurers can launch or adapt products.

Claims, on the other hand, represent the moment of truth for the policyholder. The way claims are handled shapes customer trust, operational efficiency, and the ultimate loss ratio of the portfolio.

Both processes involve large volumes of decisions, detailed rules and exceptions, interactions across multiple systems, and the need to balance speed with strong governance. As products evolve and regulations change, the underlying logic becomes even harder to manage.

The scale of claims alone illustrates the operational weight of this process. Industry studies² show that claims costs can represent up to 70% of total expenses for many insurers, making claims management one of the most critical drivers of operational performance.

Source²: https://www.mckinsey.com/industries/financial-services/our-insights/insurance

At the same time, underwriting decisions directly shape risk exposure and long-term portfolio profitability. Even small inconsistencies in pricing, risk evaluation, or policy approval can compound into significant financial impact.

Yet despite their strategic importance, many insurers still run these processes through fragmented workflows and manual interventions.

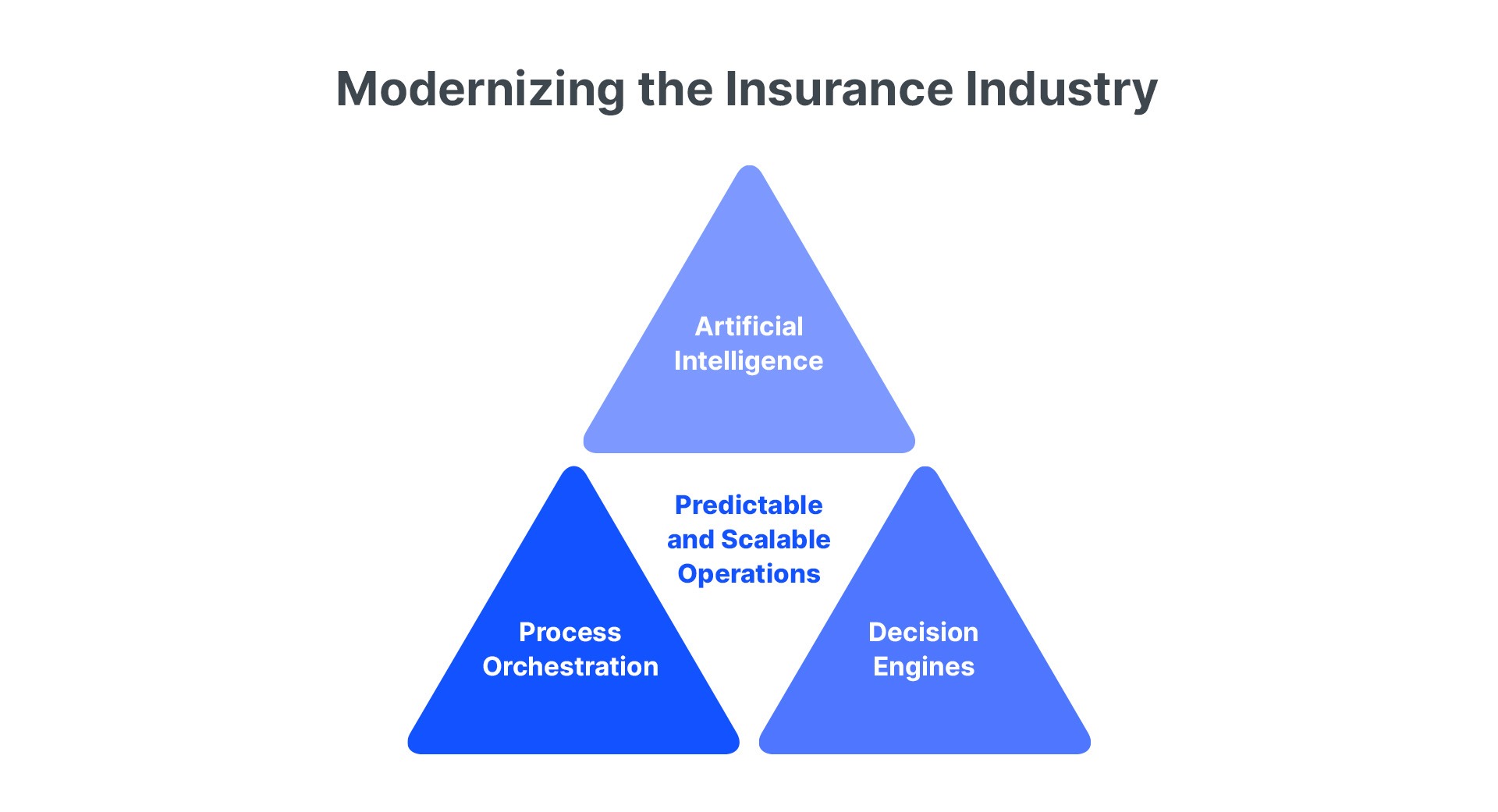

A New Operating Model for Insurance Processes

To address these challenges, many insurers are rethinking how critical operational processes are structured.

Rather than relying on fragmented workflows and manual coordination between teams, organizations are moving toward more structured and orchestrated operational models.

In this model, claims and underwriting are treated as governed digital processes rather than collections of isolated tasks.

Automation plays an important role, but the transformation goes beyond simple task automation. The focus is on orchestrating decisions, rules, and workflows across the entire process.

Key elements of this new approach include:

- Structured process orchestration across systems and teams

- Configurable rule and decision management

- Integration with data platforms and AI models

- Real-time visibility into operational KPIs and decision flows

This allows insurers to maintain strong governance while increasing operational speed.

Executives gain clearer oversight of how decisions are made.

Operational teams spend less time navigating systems and more time focusing on complex risk analysis or customer interaction. And organizations can adapt faster when regulations or products change.

From Fragmented Workflows to Orchestrated Decision Flows

One of the most significant shifts happening in insurance operations is the move from fragmented workflows to orchestrated decision flows.

Instead of relying on disconnected systems and manual coordination, insurers are designing processes where decision logic is explicit, traceable, and configurable.

In claims, this means automating steps such as policy verification, damage assessment workflows, fraud checks, and payment approvals while maintaining clear governance across exceptions.

In underwriting, it means structuring risk evaluation through transparent rules and scorecards that can be adjusted by line of business, product, region, or customer segment.

Technologies such as process orchestration platforms, decision engines, and AI-supported analytics are increasingly enabling this model.

The result is a more predictable and scalable operational environment.

Decisions become easier to trace and audit. Rules can be updated without rebuilding entire systems. And insurers can launch new products or adapt pricing strategies without reengineering the underlying processes from scratch.

Across the industry, insurers are investing heavily in operational modernization. These initiatives typically focus on:

- Automating repetitive operational tasks

- Structuring decision logic through configurable rules

- Integrating legacy systems with modern platforms

- Improving visibility into operational metrics

Claims modernization often focuses on reducing cycle times and improving fraud detection while maintaining strong governance. Underwriting modernization typically aims to accelerate policy issuance, improve pricing consistency, and enable faster product launches.

The common objective across these initiatives is clear: increase operational speed without losing control.

A Perspective from Real Insurance Transformations

At NTConsult, insurance is one of the industries where we have built the deepest experience.

Over the past two decades, we have worked with insurers across North and Latin America to modernize critical processes such as claims and underwriting. These projects often involve highly regulated environments where operational reliability, auditability, and security are non-negotiable.

Here you can see details of one of our cases:

In these scenarios, the goal is not simply to introduce new technology, but to redesign how operational decisions are structured. That means connecting legacy systems, modern platforms, and data environments into orchestrated processes where rules are transparent, decisions are traceable, and governance is embedded from the start.

Most importantly, it allows organizations to scale their operations without accumulating additional complexity. And in a market where operational efficiency and risk management are closely tied to profitability, that shift can become a powerful competitive advantage.